Insurers indicate higher premiums for residents of Tier 1 cities amid rising healthcare costs and pollution-linked risks

Dateline: New Delhi | 8 November 2025, Asia/Kolkata

Summary: Insurance companies in India are reportedly preparing to increase health insurance premiums for policyholders living in metro and Tier 1 urban centres. The move reflects higher claim costs, accelerated medical inflation, elevated pollution- and lifestyle-disease risks in major cities. The development marks a shift from the traditional one-size-fits-all premium model and signals rising cost pressure on urban households.

1. What insurers are saying and what the change means

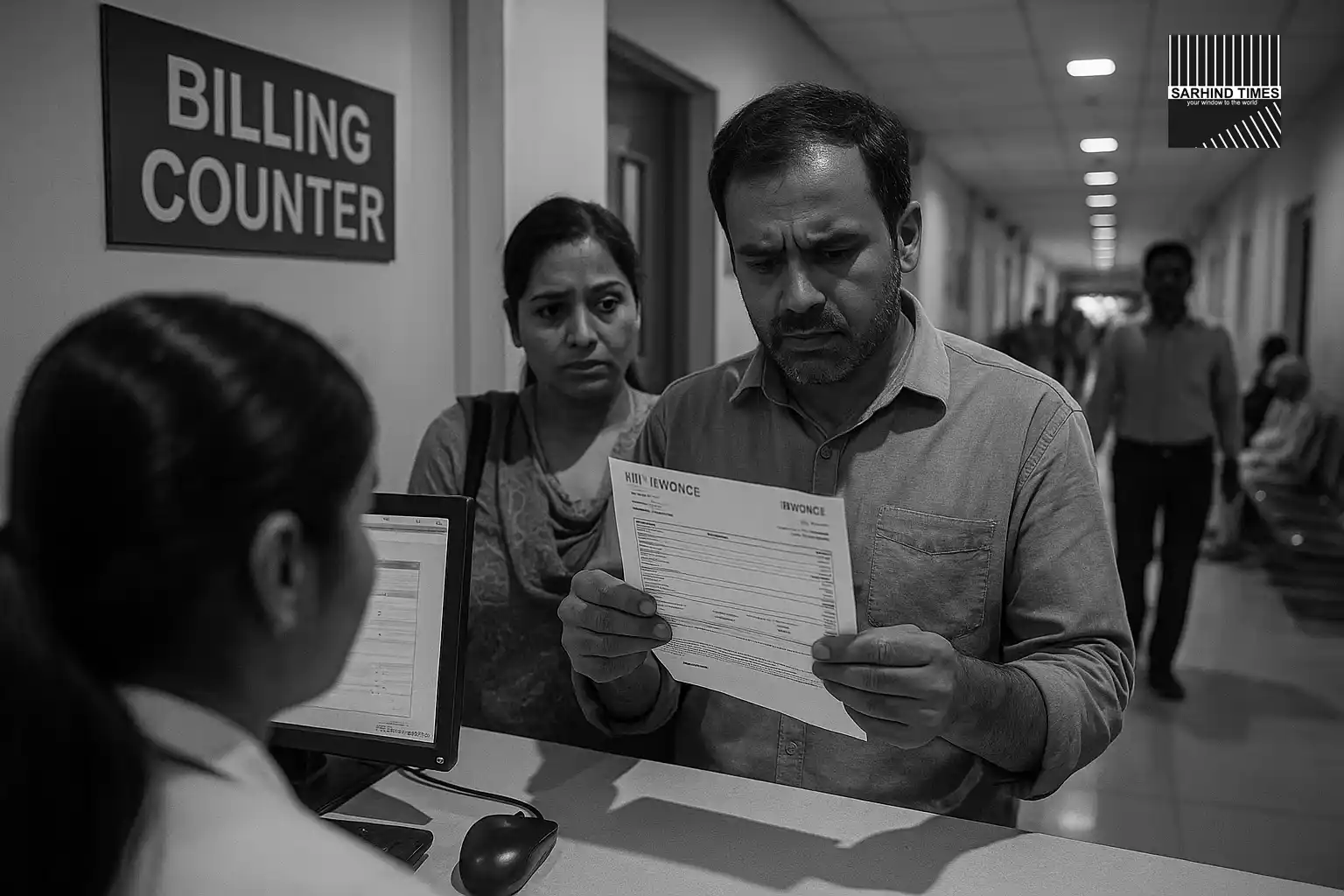

Recent industry commentary indicates that insurers are revisiting their premium-pricing models to factor in city-based risk differentiation. Residents of large metropolitan centres such as Delhi, Mumbai, Bengaluru and other major Tier 1 cities are especially in focus. One insurance-industry expert noted that premiums may rise for metro residents as “the cost and risk environment” differs sharply from smaller towns.

While exact premium-hike percentages are not yet uniform across companies, the message is clear: urban policy-holders should expect a price adjustment when their plan renews. For many households in major cities, this marks a departure from relatively stable renewal rates of past years, and introduces new budgeting pressures.

2. The driving forces: Why metro premiums are under pressure

A combination of structural factors drive the premium pressure:

- Higher medical treatment costs in metro multi-specialty hospitals: Equipment, room rents, specialist fees, advanced procedures cost more in urban centres.

- Elevated claim incidence in cities: Lifestyle diseases (hypertension, diabetes, obesity) are more common in metro populations, increasing long-term risk for insurers.

- Environmental and pollution burden: Major cities face higher levels of air pollution and environmental stress, which contribute to respiratory and cardiovascular claims—adding to insurer risk calculus.

- Medical inflation acceleration: Healthcare costs in India are rising faster than general inflation—in some analyses projected at ~13 % for 2025; insurers cite this as a core cost driver.

The result: insurers feel compelled to segment premiums based on geography and risk-profile rather than apply uniform rates across urban and rural zones.

3. Implications for urban households and policy-holders

The upcoming premium revisions will have real-world effects:

- Budget impact for metro families: An urban household renewing health insurance may face tangible increases—this squeezes family-budgets already grappling with inflation, housing & educational costs.

- Decision dilemma on coverage vs cost: Faced with higher premiums, policy-holders may reduce sum-insured, shift to lower-tier plans, or even postpone renewal—an undesirable reaction from a risk-management perspective.

- Regional inequality of cost: While rural and smaller-city residents may continue under lower premium regimes, urban dwellers will feel the cost-differential—raising questions of affordability and access in major metros.

- Renewal timing matters: Policy-holders with renewals scheduled soon should proactively review their plans, check for upcoming premium-adjustments, and compare alternatives rather than passively accepting renewal terms.

4. How the insurance industry is responding and adjusting

Insurers are taking multiple operational and product-design steps in response:

- City-tier rating models: Insurers may adopt premium loading based on geographies with higher hospital-costs and claim-freqencies.

- Underwriting & segmentation refinement: Urban policy-holders may face more stringent underwriting, higher waiting periods, and more premium differentiation based on lifestyle indicators or location.

- Cost-containment focus: Industry and regulators are exploring stricter hospital rate-control mechanisms, improved claim-monitoring and use of digital-claim exchanges to manage cost escalation.

- Product innovation: Insurers may launch city-specific health-plans, premium-tiers linked to location, or wellness-based discounts for urban policy-holders who manage lifestyle risks.

5. The regulatory and policy environment

The move comes amidst regulatory scrutiny of cost escalation in health insurance. For example, the Insurance Regulatory and Development Authority of India (IRDAI) and the government are preparing enhanced oversight of the national health-claims exchange to curb inflated hospital charges and claim-payments, which feed into premium hikes.

Also, while the government has introduced favourable tax/treatment reforms—such as exempting health-insurance premiums from GST from 22 September 2025 to ease cost for policy-holders—this contrasts with the rising underlying premiums for urban dwellers.

The regulatory pull-on-costs and insurer response create a dynamic environment where urban risk-factors, cost-inflation and product-design are converging.

6. What to watch: indicators and triggers

Key metrics and developments to monitor for urban policy-holders and insurers include:

- Announcements of premium-scale increases by major health-insurers for metro tiers, their quantum and justification.

- Change in waiting-periods, sub-limits or exclusions applied specifically to urban plans or higher-risk segments.

- State-level hospital room-rent / tariff regulation changes in urban hospitals, as tariffs drive insurer costs.

- Urban-pollution and lifestyle-disease metrics: if environment or health trends worsen, insurers may accelerate pricing adjustments.

- Renewal-behaviour: number of policy-holders dropping coverage or shifting plans after premium hikes could signal cost-shock and access issues.

7. Strategic advice for policy-holders (you, Vasu, and others)

As someone focused on income generation, content-creation and financial planning, these trends imply practical steps:

– If you live in a metro city (like Gurugram, Delhi-NCR area) check your upcoming renewal—anticipate an increase and factor it into your budget.

– If premium increases are steep, compare alternate insurers/plans; moving early may secure better terms before further hikes.

– Review your sum-insured: urban healthcare cost is rising, so lower cover may become inadequate—balance cost vs adequacy.

– Consider wellness-linked or lifestyle-incentive health policies—insurers may offer urban-discounts if you meet preventive metrics (non-smoker, gym-user, etc.).

– Track your hospital network: in metros, use network-hospitals with negotiated rates; avoid out-of-network unless necessary.

– For content creation or business households, consider group-health plans or cross-coverage options that may offer cost-leverage.

8. Broader implications for the urban ecosystem

The shift has wider consequences:

– Urban-living costs just got another dimension: healthcare insurance may become a larger fixed cost for urban households, affecting disposable income.

– Real-estate and urban-migration decisions may weigh healthcare-cost-proximity and insurance-premium-impact more heavily.

– Insurers may accelerate product-design for cities: more customised plans, wellness-features, premium-tiers. This could widen access-divide between urban and semi-urban/rural plan-costs.

– Policymakers may face pressure to cap hospital-tariffs, regulate hospital-room rents or manage pollution/lifestyle-risks if insurance affordability becomes a public-policy issue.

9. Risks and uncertainties in the trend

This premium-increase trend is not guaranteed across all insurers or cities—some variables and uncertainties remain:

– Some insurers may absorb cost-increase through operational efficiencies rather than passing it fully to policy-holders.

– Urban families may push back, select smaller sum-insured or skip renewal, which could change insurer risk-calculations and slow premium hikes.

– Regulatory intervention (tariff caps, hospital-rate regulation) may limit premium hikes if consumer-access concerns escalate.

– The magnitude of premium increase is unclear; while risk-differentiation is logical, severe hikes could spur policy drop-outs or adverse selection— insurers will need to manage carefully.

10. Conclusion: urban health-insurance cost turns major concern

The prospect of higher health-insurance premiums for metro residents marks a turning point in India’s insurance-market dynamics. As urban living costs rise, lifestyles change and medical treatment becomes more expensive, insurance companies are moving from broad-base pricing to more refined risk-based segmentation. For urban households, policy-holders and entrepreneurs, the simple message: healthcare coverage just became more expensive—and staying ahead of the change will matter.

Given your focus on income and financial planning, factor this trend into your budgeting, review your coverage early, and use this period of change as an opportunity to reassess your insurance strategy before costs rise further.

+ There are no comments

Add yours